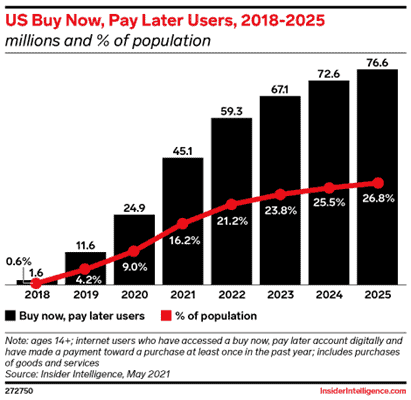

Since the start of the pandemic, young shoppers have been propelling ‘Buy Now, Pay Later’ (BNPL) technologies to finance’s front lines. According to Insider Intelligence, the number of consumers using BNPL applications will jump from 1.6 million in 2018 to close to 60 million by the end of this year. And with companies like Apple joining in on the payments game, this number is going to continue climbing as we head toward 2030. But what are the risks with this technology, and where will potential disputes in the space lie as regulators attempt to mitigate market risk?

Buy Now, Pay Later By the Numbers

In order to understand the trajectory of the market, it is important to see exactly how this service stands with consumers in the payment systems market. So, we first ask: why do consumers use BNPL services? CBInsights reported that two of the most cited reasons highlight avoiding credit card interest and making out-of-budget purchases.

Let’s look at some of the key statistics defining the industry today:

- More than 70% of consumers reported that they have heard of BNPL services

- 38% of digital buyers in the US used BNPL technology last year

- BNPL is predicted to reach $1 trillion in annual gross transaction value by 2025

These users can sign up with BNPL platforms with ease, allowing for widespread adoption as many services don’t perform ‘hard’ credit checks. In other words, to consumers, buy now pay later = guaranteed approval. The platforms typically offer a timeline of payment installments ranging from four payments split into two weeks to a single lump sum, interest-free payment at the end of 30 days with spending capabilities starting at a few hundred dollars and spanning upwards of five figures. So, who is garnering the most attention from consumers in the space today?

Top Players

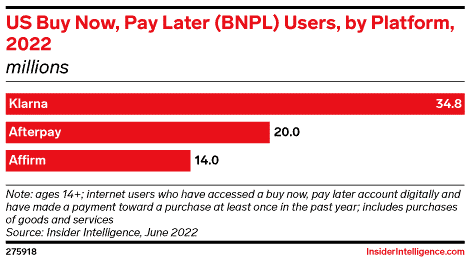

Who are the leading buy now, pay later apps in the industry? Affirm, Afterpay, Zip, PayPal’s ‘Pay in Four’, and Klarna are consumers’ top picks in the space, but that is sure to be shaken up after Apple launches their own BNPL system, Apple Pay Later, which is slated to debut this fall. These top players seem to be creating new partnerships with traditional banks and merchants every day, expanding consumers’ purchasing capabilities to cover everything from food to clothing to cars. And now, major banks are also creating their own BNPL applications like Visa Ready in order to capitalize on the fact that more than 40% of consumers would prefer to use BNPL options from their banks instead of alternative companies.

Apple is around the 80th entrant to the market vying for a piece of this BNPL pie, and this number doesn’t even include banking institutions attempting to activate their own BNPL options. This is up from 67 providers in the space last year; with the market expanding at this rapid rate, many financial forecasters are beginning to worry about the implications of this seemingly simple software.

The Ongoing Risks and Incoming Regulations

When it comes to risk, one thing is for certain: younger consumers, typically those between the ages of 18-34, are taking hold of this technology. Gen Zers and Millennials are making up 61% of the market share, and they also are the most vulnerable when it comes to the financial risks associated with this type of spending.

This technology is prompting precarious purchases from consumers. Let’s examine where these platforms are falling short in the realm of consumer protection:

- More than 1/3 of those using BNPL services had missed at least one payment

- Nearly 70% of BNPL users admit to spending more than they would have if they were required to pay in full upfront

- According to a Credit Karma study, more than half of Gen Z and Millennial respondents who have used BNPL services say they have missed at least one payment, compared to 22% of Gen X and just 10% of Boomers.

Since the size of these services began ballooning, regulators have taken notice as the amount of debt held by the platforms continues to rise. The industry has essentially been free of regulations- until now. The US Consumer Financial Protection Bureau (CFPB) announced its BNPL inquiry last December to investigate how major players are collecting, maintaining, and distributing data. They also took issue with BNPL users’ risk of being caught in a cycle of debt through multiple ‘pay later’ purchases, and the presence of regulatory arbitrage.

This points to incoming regulations regarding “aggressive origination and underwriting practices, inadequate disclosures, and unpredictable credit reporting practices” as highlighted by the American Bankers Association (ABA). The ABA along with a slew of lawmakers believe that regulations that relate to basic consumer protections will make BNPL a great option for those looking for point-of-sale credit. As the ABA stated in their letter to the CFPB: “These safeguards include clear disclosures, including with respect to repayment obligations, the cost of credit, and consumer rights; the ability to effectively report BNPL payment behavior, which will support building credit and responsible underwriting; and clear disclosure by BNPL providers of their data collection and data use practices.”

Additionally, the introduction of the Fed’s recent interest hike and ongoing inflation made us wonder: will more people be pushed toward BNPL technology, helping propell forward the potential for a recession? According to WIT affiliate expert David X. Martin, the BNPL market is currently too small to affect the potential for a recession, even with its exponential growth. Martin explains that “I think that inflation could end quickly-without a bruising recession- when there is joint fiscal, monetary, and economic reform. However, without these reforms, the threat of a recession is real and will cause more people to be on the fringe to adopt BNPL technology.”

Potential for Litigation

Some of the major players in the space have already been involved in disputes over issues involving consumer protections; Klarna has been hit with multiple class actions after plaintiffs claimed that the app had deceived users about the true risks associated with the service, claiming it preyed on poor shoppers struggling to make ends meet. Martin feels that similar fraud claims under state consumer protection will likely soar in the coming year. There will likely be an uptick in class action suits alleging that companies offering BNPL options fail to disclose to customers unfavorable loan terms and the risk of incurring significant fees if customers fall behind on payments. But these conflicts won’t be the only problems facing those fighting for their space in the buy now, pay later race.

As more providers begin to hit the market, many will be creating their own proprietary systems, attempting to set themselves apart from the crowd. This will create conflict over software and intellectual property licensing agreements for their technology, prompting IP disputes in the space. And while some regulations may offer a sense of standardization in the industry, much of this software will have different approaches to financing, making regulators tread lightly when it comes to the implementation of sweeping guidelines.

No matter the issue, WIT has a team of payment systems experts prepared to address incoming disputes in the space. Our affiliates include…

- Former banking executives who understand banking policies, standards, and compliance

- Payment processing specialists with expertise in SWIFT, payment rails, and point-of-sale (POS) transactions

- Fintech software engineers who know open banking technology, apps, and APIs

- Digital transaction specialists with knowledge on mobile deposits, smart cards, and digital wallets

- Cryptocurrencies experts who understand virtual currencies and exchanges

- Former investment banking insiders who know decentralized finance (DeFi) and smart contracts

- Computer scientists with expertise in biometric technology, data security, and cryptography

Want more insights on what’s to come in finance and payment systems? Reach out to WIT for the best experts to inform your litigation strategy. Our expert teams were created to address what we expect to be the key areas of litigation in emerging technologies like buy now, pay later. Follow us to stay up-to-date on what is to come in the future of the financial technology industry, and contact us to learn more about our partner briefings.